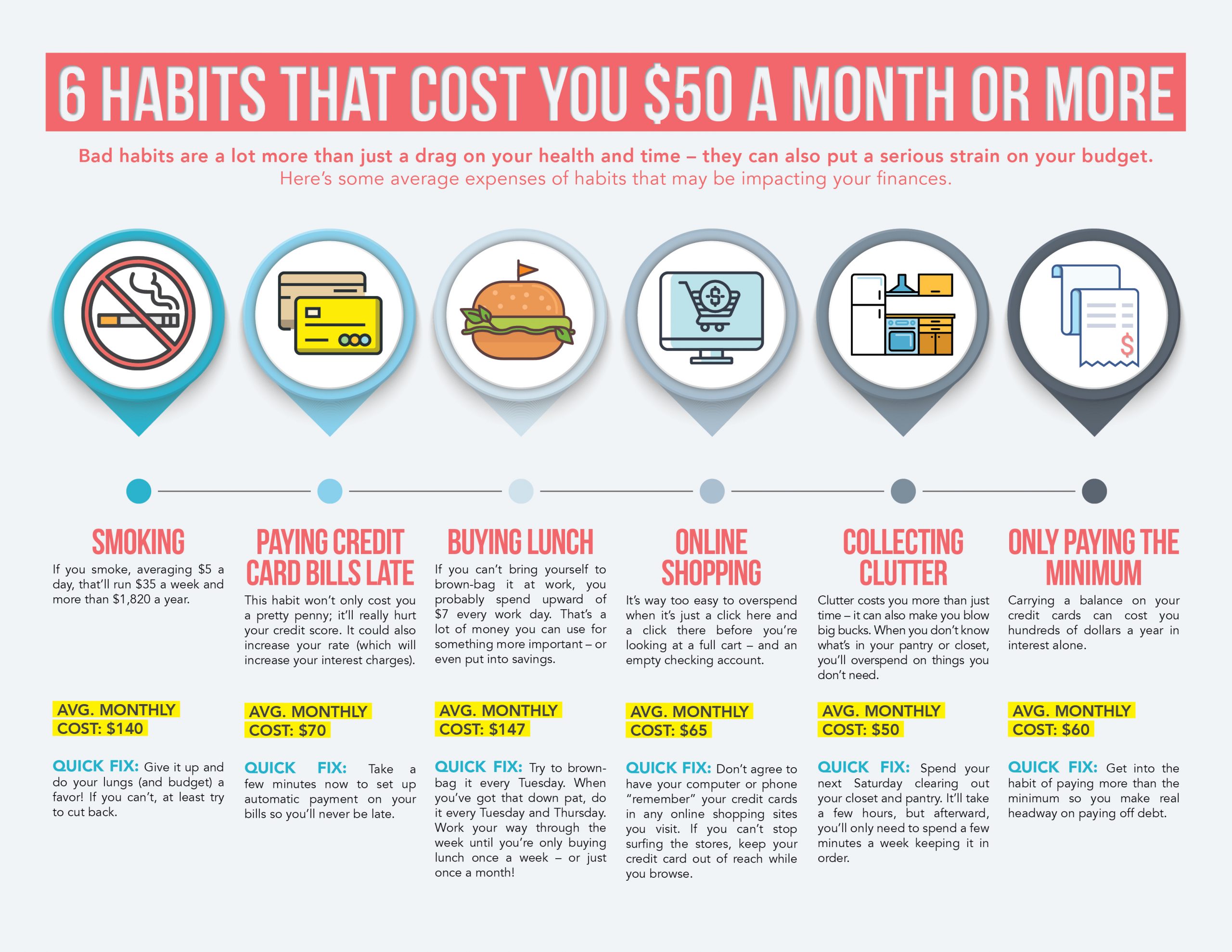

6 Habits That Cost You $50 A Month Or More

April 1, 2020

Beware the 2020 Census Scam!

April 15, 2020

Q: Since the coronavirus has landed on American shores, each day seems to bring more devastating news about the state of our economy. What steps should I be taking to protect my personal finances during this time?

A: The coronavirus outbreak has already generated severe consequences for the national and global economies — and experts say we’re only seeing the beginning of the pandemic’s financial fallout. The virus ended one of the longest bull markets in history, as the stock market plunged by a full 25 percent in one volatile month. In fact, it saw its worst day since 1987. More than that, businesses have been adversely affected by the outbreak in many ways: production lines have been put on hold as the delivery chain is disrupted indefinitely; the global-wide halt on travel has caused tremendous losses for the tourism and airline industries; sports and entertainment industries have taken huge hits; and countless other business lines have been negatively impacted by a dearth of supplies, decreased spending and a shortage of personnel due to quarantines or school closures.

With all this uncertainty, it’s easy to fall into a panic and wonder if there are some concrete steps you should be taking to save your personal finances from impending ruin. Here are some practical dos and don’ts to help you maintain financial stability and peace of mind during this time.

Don’t: Panic by selling all your investments

Both seasoned investors with robust portfolios and those simply worried about their retirement accounts can find it nerve-racking to see their investments drop in value by as much as 10 percent a day. It may seem like a smart idea to sell out just to spare investments from further loss, but financial experts say otherwise. According to The Motley Fool, most sectors of the economy will recover quickly as soon as the outbreak clears. For example, consumers may not be purchasing shoes or cruise tickets now, but they will likely do so when it is safe to shop and travel again. While the global and national economy may not bounce back for a while, experts are hopeful that individual business sectors will recover quickly.

Do: Trim your spending

The thriving economy the country has enjoyed for a while has prompted a gradual lifestyle inflation for many people. As the economy heads toward a probable recession, this can be a good time to get that inflation in check. Work bonuses, raises and promotions are not handed out as freely during a recession as they were in recent years. Some people may even find themselves without a job as companies are forced to lay off workers in an effort to stay solvent. Trimming discretionary spending now can be good practice for making it through the month on a smaller income. It’s also a good idea to squirrel away some of that money for a rainy day.

Don’t: Put your money before your health

Financial wellness is important, but physical health should always take priority. If you’re feeling unwell, and especially if you’re exhibiting any of the symptoms of the coronavirus — such as fever, coughing and shortness of breath — call in sick to work. Do the same if you’ve been exposed to someone who has tested positive for COVID-19 in the past 14 days. Don’t let financial considerations come before your health and the health of those you come into contact with each day.

As part of a package of executive orders to help mitigate the financial fallout of the coronavirus, President Donald Trump has announced that all employees are entitled to two weeks of full paid leave if they are unable to work because of the coronavirus. This includes contracting the actual virus, self-quarantining for fear of having been exposed to the virus and caring for a family member who has contracted the virus, or for children who are home due to school closures. Be sure to take advantage of this offer by making your health paramount.

Similarly, doctor visits can cost a pretty penny, but when necessary, should always outweigh financial concerns. A co-pay or insurance deductible is a small price to pay for your health.

Do: Consider a refinance

The silver lining of an economic environment like this is falling interest rates. As of March 17, the average interest rate on a 30-year fixed-rate mortgage is 3.3%, down from approximately 4.5% of a year ago. Refinancing an existing mortgage at this lower rate can potentially save homeowners several hundreds of dollars a month. That extra breathing room in a budget can be a real boon in case of salary cuts or even a layoff during a recession.

Be sure to work out the numbers carefully before considering this move since a refinance isn’t cost-free. Contact TVACCU to learn about your options.

The coronavirus has already impacted the economy tremendously, and will likely continue to do so for a while. Keep your own finances safe by remaining calm, putting your health first and taking some of the practical steps mentioned above.

{kind=link}